March 16, 2026 · 5 mins read

Santosh Kumar

Your score can occasionally dip after you pay off a loan or credit card balance because the credit mix shifts, older accounts close or lenders refresh account status in the report. In the majority of instances, this decrease is short-lived and the score stabilizes after the credit profile refreshes.

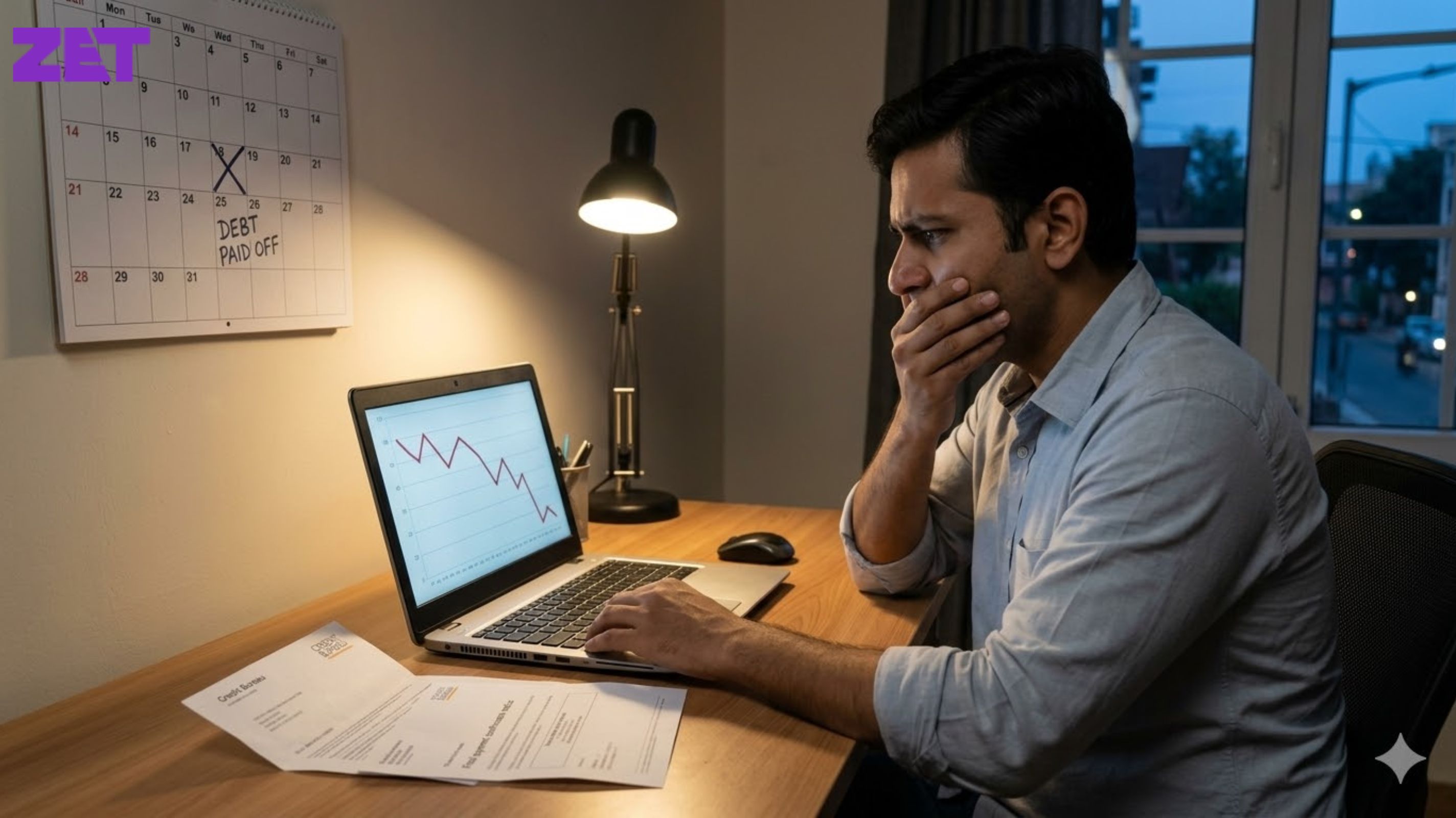

Most folks think paying off debt will automatically raise their credit score. Yes, paying off debt is fiscally prudent, but credit scoring formulas look at many variables other than repayment.

In India credit scores are determined through information banks and financial institutions report to credit bureaus like TransUnion CIBIL. These reports cover information on existing loans, credit cards, repayment habits and credit profile.

When a loan is fully repaid, the lender modifies the account status on the credit report. During this update process, some scoring factors can temporarily shift, causing a short term drop in the score.

That typically doesn’t mean bad financials. Instead, it mirrors changes in the credit profile.

A common culprit of a score drop is a shift in the borrower’s credit mix. Credit scoring models like to see a good mix of secured loans, unsecured loans, and credit cards.

When a loan closes upon repayment, the credit profile may suddenly lack active credit accounts. This can limit the mix of credit types on the report. Say for instance, you had a personal and credit card and the personal loan gets closed, then your credit mix is reduced. This could cause the score to dip a bit until new credit action layers up a fresh profile.

Another potential influence on the score is the age of credit accounts. Credit history length is a big factor in credit scores because, typically, longer histories mean better scores.

If the repaid loan was among the oldest accounts on the credit report, then closing it could lower your average age of credit history. This can temporarily bring the score down.

Credit history length is also a significant factor in credit scoring models used by TransUnion CIBIL.

Credit Factor: Credit Mix

Possible Impact After Loan Closure: Fewer types of active credit accounts

Credit Factor: Length of Credit History

Possible Impact After Loan Closure: Average age of accounts may decrease

Credit Factor: Account Status Update

Possible Impact After Loan Closure: Temporary scoring adjustments

Credit Factor: Credit Utilisation Ratio

Possible Impact After Loan Closure: May change if credit cards are heavily used

Also Read: Annual Fee vs Lifetime Free Cards

If your credit score slips post-debt payoff, there are a few easy measures you can take to steady it and boost it once more.

First, keep paying all credit card bills and EMIs on time. Regular repayment habits is the strongest credit profile reported by TransUnion CIBIL.

Second, maintain a low credit card utilisation. Utilizing a significant part of the credit limit harms the score. Preferably, keep utilisation under 30 per cent of the credit limit.

Another helpful measure is to keep at least one open credit account. Good credit card usage keeps the wheels of credit activity turning, which is a bonus for your score.

Also Read: GST for E-Commerce Sellers: Rules & Compliance Checklist

You should also review your credit report every once in a while and make sure that the closed loan is marked as “closed,” not “settled” or “written off.” And then, of course, incorrect status updates can also hurt your score — and should be rectified with the lender if need be.

In general, credit scores rebound naturally over a few months provided repayment behaviour is consistent and credit utilisation is managed.

Although short term score fluctuations are possible, the main objective should be preserving a healthy credit profile in the long run.

Borrow responsibly, a.k.a. pay your bills, don’t take out frivolous loans and check your credit reports regularly.

Also Read: What Is GSTIN? Format, Structure, and Meaning Explained

Having a good credit score can increase your approval likelihood for crucial financial products like personal loans, home loans, and credit cards. It can also assist borrowers in obtaining reduced interest rates from lenders.

By prioritizing consistent financial discipline over immediate score shifts, people can keep a credit profile that's stable and dependable.

The credit score will begin to stabilise within a few months after closing the loan, assuming that the lender continues to report positive repayment activity during this time.

No, paying off closed loans is a good thing to do, and there are usually temporary negative impacts associated with doing so.

You can check your credit report from TransUnion CIBIL to see if your loan closure was reported properly.

Build and Maintain a 750+ Credit Score